Executive Summary

Ledger-based carbon accounting is a novel approach to tracking where, when, and how greenhouse gas (GHG) emissions are released in the production of goods and services. It enables decision-makers in business, financial markets, and governments to meet emissions reporting requirements, weigh investments and purchases, and drive decarbonization efforts. Ledger-based accounting introduces an accurate, consistent, and efficient system for calculating and sharing emissions information. The use of ledger-based accounting, either by itself or in conjunction with existing approaches, enables the providers of goods and services to better identify, prioritize, and accelerate the actions needed to reduce emissions.

For businesses, ledger-based carbon accounting can strengthen corporate operations, reputations, partnerships, and international competitiveness. The ledger-based system can also unlock new capital flows within financial markets and introduce greater precision in risk assessment for investors. Finally, ledger-based accounting can provide a more complete emissions picture for policymakers, driving more effective policy- and decision-making and ultimately leading to greater and faster emissions reductions.

Introduction

Carbon accounting refers to the measurement, allocation, and tracking of GHG emissions in the production of goods and services. Effective carbon accounting details where, when, and how emissions are released. As such, it is the foundation for all actions to address GHG emissions. Entity-level and economy-wide emissions data enable businesses and policymakers to understand the extent of emissions from a particular sector or company, providing visibility into the amount of emissions associated with certain kinds of activity. By contrast, product-level emissions data allow companies to track the emissions associated with their goods and services at each step in the supply chain.

While familiar GHG reporting approaches like the Greenhouse Gas Protocol may assign the same emissions to multiple actors to capture the full emissions impact of a sector or activity, under a ledger-based accounting framework, all anthropogenic (in other words, human-caused) emissions are counted once and only once and are fully allocated to the entity or entities responsible for generating those emissions. When all emissions are counted only once and fully allocated, it is clear which entities have responsibility for specific emissions streams.

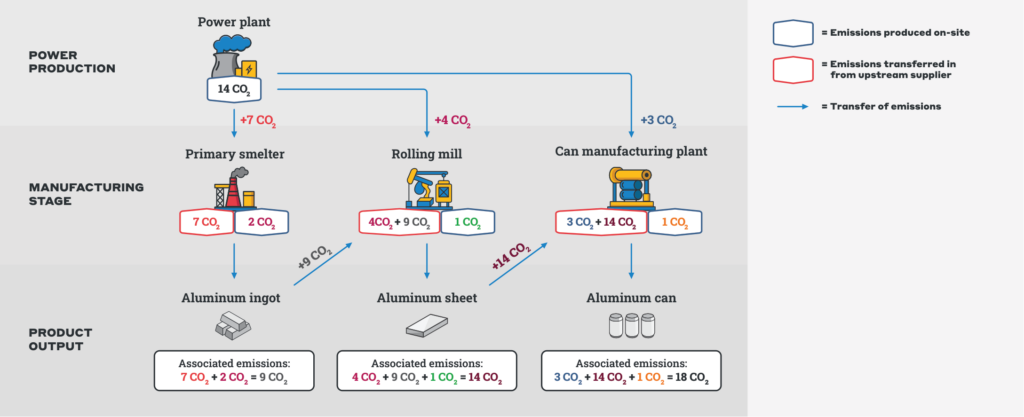

In the ledger-based system, companies account for all their direct, on-site GHG emissions and removals (meaning drawdowns of GHGs from the atmosphere). Companies then add in the emissions and removals embedded in products and services purchased from immediate suppliers to determine their total emissions. At each stage of production, these upstream and on-site emissions are allocated to the emissions ledgers of individual goods and services, enabling the calculation of product-level emissions, as in Figure 1 below.

Figure 1. Illustrative example of ledger-based carbon accounting from the aluminum supply chain.

This figure illustrates the transfer of emissions in the hypothetical production of ~1 ton of aluminum cans using ledger-based carbon accounting. Emissions are passed from facility to facility alongside the transfer of power or material inputs. At each stage in production, a share of upstream and on-site emissions is allocated to thecarbon dioxide ledger of the emerging product. Note that this figure is simplified to exclude additional fuel and material inputs.

Existing corporate reporting regimes like the Greenhouse Gas Protocol have been used for decades to estimate GHG emissions, and they remain important tools for assessing emissions performance across corporations’ full value chains. However, ledger-based accounting is needed to meet market and policy conditions that demand greater precision in determining the actual GHG emissions being released at any given point across entire supply chains.

The Bipartisan Policy Center views robust and accurate carbon accounting as a critical foundation for effective climate and trade policy, well-functioning carbon markets, and the development of a market for differentiated oil and gas. For more information, see our carbon accounting explainer and our article on the difference between carbon accounting and reporting.

Key Features of Ledger-Based Accounting

A ledger-based accounting framework offers three foundational qualities that benefit companies, investors, and governments alike.

- Accuracy. A key feature of ledger-based carbon accounting, accuracy in emissions measurement is crucial to creating accountability and providing reliable and actionable information. The ledger-based system minimizes errors and prevents them from propagating as information is passed down a supply chain. Because facilities are responsible for counting only their own emissions, there is a clear chain of custody for emissions data. Verifiers can then trace each emissions figure across the supply chain, reinforcing the accuracy of the emissions data.

- Consistency. A standardized approach for collecting, calculating, allocating, and reporting emissions data is necessary for true comparability across products and companies. When companies follow the same accounting rules, customers can reliably compare emissions profiles across potential suppliers, investors can evaluate the merits and trade-offs of low-carbon investments, and governments can determine where policy action is most needed and track progress once action is taken.

- Efficiency. A ledger-based system streamlines data management while maintaining data confidentiality. New technologies can support this process by automatically tracking and transferring emissions data as products move through the value chain, ensuring that information remains accurate, traceable, and auditable at every step. In this way, entities can gain contractual, easy, and reliable access to upstream emissions data.

Distinguishing Ledger-Based Accounting From Other Reporting Practices

As noted above, existing corporate reporting practices like those established by the Greenhouse Gas Protocol remain important for assessing entity-wide emissions, including the impacts of their products and services once those products and services leave their control. By design, the GHGP asks companies to estimate the emissions released outside of their direct control but within their supply chain, either from an upstream manufacturer that supplies a particular input or by a downstream customer that uses the company’s product. This encourages companies to consider supply-chain-wide emissions and can help policymakers see which sectors have the greatest impact on overall emissions.

Other initiatives, such as the Partnership for Carbon Transparency, are focused on improving and standardizing product-level carbon footprints to better approximate how emissions are transferred between facilities when a material is sold from one manufacturer to another. While these product-level frameworks improve comparability across products, they do not enable comprehensive carbon accounting across industries and economies.

The Case(s) for Ledger-Based Accounting

By lending greater accuracy, consistency, and efficiency to emissions collection and allocation, ledger-based accounting can complement and enhance existing approaches, ultimately facilitating accounting at the economy, entity, and product levels. These attributes translate into specific benefits for corporate actors, financial markets, and governments. The sections below describe how ledger-based accounting benefits each of these groups.

1. The Business Case: Reducing Costs and Boosting Confidence

Businesses need carbon accounting to satisfy customer demands, meet corporate commitments, and, in some cases, demonstrate low-emissions performance to gain a competitive advantage. Current reporting standards check some of these boxes, but in all instances, the ledger-based approach enables greater accuracy, consistency, and efficiency.

Ledger-based emissions accounting improves GHG reporting in four particular ways, yielding major advantages for businesses:

Lowering costs by reducing administrative inefficiencies while still protecting confidential business information

Providing reputational advantages by building trust between partners and bolstering the integrity of environmental claims

Allowing businesses to more accurately compare the emissions embedded in material inputs

Making it easier for businesses to access product-level emissions data to comply with emerging trade requirements

A. Lower Costs: Reducing the Administrative Burden of Data Collection

Under a ledger-based accounting framework, suppliers transfer emissions data to buyers when products or services are sold. As a result, companies no longer need to make generalized estimates for their upstream emissions or contact each of their suppliers individually for more precise data. This cuts down on administrative costs for large and small companies alike by streamlining the emissions data collection process.

A coordinated system for emissions data can be designed to protect confidential business information and ensure that after a financial transaction is completed, only the relevant emissions data would be visible to the purchasing company.

B. Reputational Advantages: Building Trust and Transparency for Corporate Partners

Without common standards, errors in carbon reporting are pervasive. Companies sometimes omit or double-count emissions when reporting to downstream partners, undermining the credibility of emissions reporting. For companies and investors that care about the environmental attributes of their purchases, the ledger-based system provides a means of introducing consistent and auditable carbon accounting practices. A clear chain of custody for emissions makes it easier to verify emissions reports and more difficult to obscure emissions sources.

C. Comparability in Decision-Making: Ensuring That Environmental Premiums Are Worthwhile

When companies use flexible carbon accounting standards, their downstream customers are forced to compare apples to oranges in their purchasing decisions. Moreover, a flexible framework creates an incentive for companies to report the lowest emissions figures possible rather than the most accurate. Consistency in carbon accounting standards, a key quality of a ledger-based framework, allows downstream businesses to easily compare goods and services.

Most corporate reporting practices employ a “scope” taxonomy that divides a potential input’s emissions into three different buckets: scope 1 (direct, on-site emissions), scope 2 (power generation emissions), and scope 3 (indirect upstream and downstream supply chain emissions). Companies can use different methodologies to assign those emissions to products and services, making comparisons difficult. Additionally, facilities employ emissions factors to estimate and include emissions sources such as employee transportation and downstream end-of-life emissions. Inconsistency between standards in terms of which emissions sources should be included, and which estimates can reasonably represent these emissions sources, makes it even more difficult to compare the emissions profiles of competing goods available for purchase.

By contrast, the ledger-based system simplifies and standardizes the emissions accounting process to ensure that the emissions profiles of products can be compared on a one-to-one basis.

D. Compliance With Emissions Reporting Requirements Abroad

Perhaps the most compelling business use case for ledger-based accounting is to meet trade requirements and standards. Most prominently, the European Union’s Carbon Border Adjustment Mechanism, which took effect on January 1, 2026, requires importers to report and pay a fee for the emissions associated with production of their goods. The U.K., Australia, and Taiwan are also implementing or considering similar emissions-based import fees. Emissions calculations for these export markets can be made much simpler with the adoption of ledger-based accounting.

At present, most emissions in the United States are reported at the company-wide or facility-specific level. Complicating matters, importers to the EU need to add together all the emissions from their upstream supply chains. Even companies that do not export directly to the EU may be asked to provide the embedded emissions of their products. That is because their downstream customers need that data to calculate the upstream emissions of goods they export to the EU for CBAM compliance. When these customers cannot access upstream emissions information, the EU will assign their exports punitive default values that overstate the true emissions of U.S. products.

Ledger-based accounting can help U.S. companies to receive recognition for their low-emissions practices in foreign markets in two primary ways. First, as previously discussed, ledger-based accounting can make it more efficient and less expensive for U.S. producers to access their upstream emissions data. Second, international markets are more likely to recognize the legitimacy of emissions calculated via a framework that is internally consistent. Consistency is a key feature of the EU’s monitoring, reporting, and verification framework, and ledger-based accounting is built for consistency.

2. The Financial Market Case: Advantages of Ledger-Based Accounting for Financial Markets

Ledger-based carbon accounting is modeled after the U.S. Generally Accepted Accounting Principles for financial accounting. As such, it helps translate emissions measurements into terms familiar to financial markets, bringing greater clarity, consistency, and trust to the transfer of emissions data. As investors increasingly evaluate companies with both financial and environmental goals in mind, traditional emissions reporting practices are insufficient to provide investors with confidence that projects intended to reduce carbon emissions are delivering an acceptable return on investment.

The ledger-based approach applies the discipline of financial accounting to carbon accounting practices, creating a transparent and verifiable record of emissions transfers across a supply chain. By establishing a common, auditable method for carbon accounting, ledger-based accounting enables markets to determine and track “what counts” in terms of emissions outcomes. This increased certainty can unlock new capital flows toward lower-emissions projects and investments and allow investors to assess related risks with greater precision.

A. Increased Credibility and a Safer Return on Investment

In the absence of common reporting standards, accounting and reporting inconsistencies erode the reliability of corporate disclosures and introduce uncertainty into asset valuations and risk models. A standardized, ledger-based accounting framework enhances market transparency and gives financial institutions more confidence in the value of their investments in a market that increasingly values lower emissions.

A ledger-based accounting system also reduces information asymmetry, mitigates reputational risk, and supports more accurate capital allocation for investors seeking environmentally credible assets. With ledger-based accounting, financiers assessing or investing in low-carbon projects can trust that their environmental investments are delivering what has been promised.

B. Closer Linkage Between Carbon and Financial Markets

Translations between carbon markets and financial markets are currently inconsistent. The adoption of a ledger-based accounting framework can provide a common, agreed-upon, and verifiable way of figuring out and tracking “what counts” in terms of activities that avoid, reduce, or remove GHG emissions. Such a framework can also account for carbon projects with different durations, addressing existing issues of comparability, permanence, and fungibility. Clearer rules of the road can catalyze new investment by market players that have been waiting on the sidelines due to credibility concerns or accounting complexities.

Moreover, the use of a ledger-based system to track and transfer carbon credits as assets would ensure that the same emissions reductions or removals cannot be claimed by multiple institutions, boosting confidence in the market and associated emissions claims.

3. The Public Policy Case: Government Applications for Ledger-Based Accounting

Finally, ledger-based accounting can assist policymakers in reducing emissions at the country, state, and local levels. By providing a clearer, more detailed view of how emissions flow through the economy, a ledger-based system can help policymakers identify and prioritize sectors and actions that would benefit from additional support or interventions. At the same time, improved precision in emissions reporting can show taxpayers that public funds are reaching projects that deliver real climate benefits. Policymakers who care about emissions reductions should see strong benefits from the use of ledger-based accounting practices across the economy.

A. Informing Effective Policymaking

For governments striving to meet decarbonization goals, ledger-based accounting provides a more complete view of emissions by sector and geography, thus giving policymakers more accurate information on which to base their decisions. Consistent state- and national-level emissions data also help policymakers determine which sectors are over- or underperforming compared to national averages or foreign competitors. This data can inform emissions-reduction tools like tax incentives and performance standards.

In particular, ledger-based carbon accounting improves government implementation of performance standards for GHG emissions. Performance standards work by rewarding producers that operate below a determined emissions threshold or penalizing operators that do not meet the threshold. Examples include clean fuel standards and product intensity standards. Consistent accounting and more accurate data let governments more easily administer performance standards and course correct as needed.

Ledger-based accounting can also support the U.S. competitive advantage when it comes to emissions-efficient production of goods and services. Access to more accurate national-level emissions data can provide an opportunity for the U.S. government to put greater pressure on its trading partners to keep pace with U.S. environmental performance while giving American goods a competitive advantage. Investigations like the International Trade Commission’s recent study of steel and aluminum emissions, for example, would have benefited from data collected via a ledger-based accounting system. Ledger-based accounting can assist in future data collection efforts to corroborate the need for trade policies that level the playing field for cleaner-operating U.S. producers.

B. Stronger Political Support for Actions That Reduce Emissions

Rigorous and accurate carbon accounting demonstrates to taxpayers the value of policies, incentives, and investments that reduce emissions. An inability to accurately assess which entities are high- or low-carbon in terms of emissions intensity undermines the government’s ability to spend taxpayer dollars on the highest-impact projects. By increasing both accuracy and transparency in carbon accounting, the ledger-based system increases taxpayer assurance that their elected officials are deploying American capital responsibly and effectively.

Conclusion

Ledger-based accounting offers a practical and scalable path to improving the integrity of emissions information across the economy and, in so doing, accelerates reductions in GHG emissions. By embedding accuracy, consistency, and efficiency into the foundation of carbon accounting, adoption of the ledger-based approach can strengthen corporate operations and supply chain partnerships, improve the precision of financial risk assessments, and equip policymakers with clearer insights into where decarbonization efforts can be most effective and how best to prioritize and design policy interventions. Implementing ledger-based accounting can not only enhance transparency and trust across markets but also unlock new opportunities for innovation, investment, and international competitiveness.

Taken together, these benefits show that modernizing carbon accounting to the ledger-based approach is not simply a technical upgrade but also a strategic imperative for companies, financial institutions, and governments working to lead in a global economy that increasingly values low-emissions performance.

{kind=link}