Market snapshot

- ASX 200: +1.2% to 8,553 points

- Australian dollar: +0.1% to 64.83 US cents, +1.3% to 102.06 yen

- Nikkei: +3% to 50,006 points

- Hang Seng: +0.2% to 25,889 points

- Shanghai: +0.3% to 3,960 points

- Wall Street: S&P 500 (+0.4%), Nasdaq (+0.6%)

- FTSE 100: -0.5% to 9,507 points

- EuroStoxx 600: Flat at 561 points

- Spot gold: -0.3% to $US4,068/ounce

- Oil (Brent crude): +0.4% to $US63.78/barrel

- Iron Ore: +0.1% to $US104.65/tonne

- Bitcoin: +2.3% to $US92,598

Prices current around 4:30pm AEDT

ASX 200 puts in strong performance post-‘Nvidia day’

The S&P/ASX 200 has closed up 104 points or 1.2% to 8,552 points.

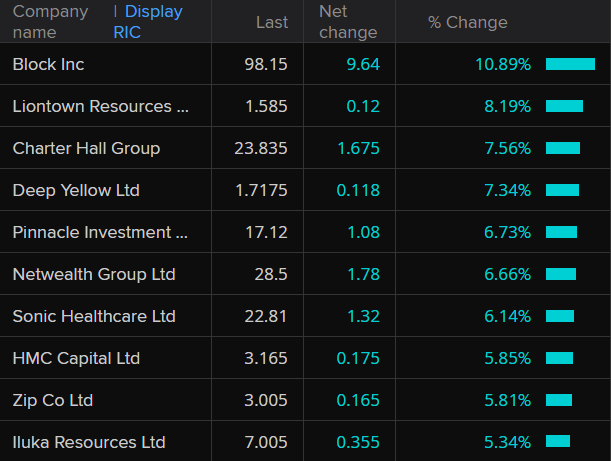

The top performing stocks in the index were Block CDI and Liontown Resources, up 10.77% and 9.73% respectively.

The index has lost 2.3% for the past five days, but it has gained 4.8% in the year to date.

Futures still going strong

Wall Street, at last check, is setting itself up for another bullish trading session.

S&P 500 futures: up 1.3%.

NASDAQ futures: up 1.8%.

Dow futures up 0.6%.

Figures at 4:10pm AEDT.

‘AI rally running on fundamentals not fumes’

An interesting short note from Thomas Matthews, the head of markets Asia-Pacific at Capital Economics:

“Recent earnings reports give cause for optimism about the health of the AI equity market rally, in our view, and we think it has further to run.”

So why does he think that?

“There have been two big questions seemingly weighing on investors’ minds lately,” he explains.

“First, will the ultimate demand for AI be strong enough to justify the enormous amount of capital expenditure currently underway?

“Frankly, it’s too soon to tell. But Nvidia’s commentary around its report (and that of the so-called “hyperscalers” undertaking the capex, with respect to their own reports) suggests that those closest to the buildout remain confident.”

The second question is whether valuations in the sector are still too high, even if the demand is there.

“One reason, in principle, for higher PE ratios might be that investors had become more optimistic about earnings more than a year ahead. If so, then the seemingly strong momentum in tech earnings at the moment, of which Nvidia is the most recent example, might help to calm their nerves, even if there is still plenty of water to flow under the bridge yet,” Matthews opines.

However, he does see one potentially imminent threat to a sustainable recovery in tech stocks.

“But there’s a separate reason for sky-high valuations this year: lower real “safe” asset yields. Indeed, by our estimate, valuations have become less stretched year-to-date when accounting for this. And it’s probably not wholly a coincidence that the recent troubles in tech started around the same time investors began paring back expectations for cuts, and yields began to rebound,” he argues.

“We think investors are still expecting too many cuts next year, too. If so, it could prove an ongoing threat to the AI rally, even if we doubt it would be nearly enough to derail it completely.”

All eyes on the ‘Takaichi trade’

Staying on the Japanese bond market, analysts have told the ABC investors are preparing for Prime Minister Sanae Takaichi to announce a huge “supplementary budget” of over 20 trillion Yen.

In simple terms, there is concern in the bond market the new prime minister will overspend, putting enormous pressure on the bond market.

The government will tap the bond market to finance its fiscal agenda.

During the recent election campaign, Takaichi promised voters she would boost the economy and protect households from rising prices.

“There is a fear in the market that the stance of the government is now pretty dovish,” chief desk strategist at Mizuho, Shoki Omor, said.

“It may be an overreaction today, but the market clearly thinks that the government is going to have to issue longer-dated bonds to fund its spending plans.”

Approaching the close…

It’s been an impressive run on the ASX 200 today… but it’s slowing as we approach the close.

The S&P/ASX 200 index is up 1.2% at 8,548 (3:50PM AEDT).

The index has gained 4.77% over the last year to date.

Not all stock markets are riding higher

While most stock markets across the Asia Pacific region are doing well, there is one exception.

Hong Kong’s Hang Seng Index is only up 0.1% to 25,867 at 3:30pm AEDT.

The Hong Kong-listed Contemporary Amperex Technology (CATL), the world’s largest battery maker, has fallen more than 8%.

It follows the expiry of a six-month sales restriction on about 77.5 million shares held by early stakeholders.

Nvidia and Australian AI

Macquarie Technology Group CEO David Tudehope claims to have a front row seat in Australian AI development.

He says NVIDIA’s positive results overnight underscore the strong fundamentals of AI, and that “Australia is slowly waking up” to the global AI opportunity.

Mr Tudehope penned this note earlier.

“When it lands fully it will bring enormous opportunities to Australia and generate wealth right across the economy.

“In our business, we not only build data centres to store and protect data, we also provide cybersecurity, cloud computing and AI services for the customers whose data we protect. This means we get to see firsthand what enterprise and public sector organisations are doing with their data, how they are increasingly adopting AI, cloud, and cyber solutions. While Australia has had a relatively slow start, this is changing.”

Afternoon update of ASX movers and shakers

David! Where’s our lunchtime market update? I’ve finished my sandwich and still haven’t gotten a summary on the movers and shakers of the morning. <3

QFE has spiked, and it looks like a lot of miners are down today.

– Charlieeee

Hi Charlieeee — Here’s your update of where the ASX is at, better late than never.

Overall, the ASX 200 is up 1.2% to 8,548 points, currently on track for its best gain since early August.

That, of course, is after suffering its worst fall since April (-1.9%) earlier this week.

Most sectors are up, with only energy and utilities in the red.

Payments provider Block is leading the top gainers on the ASX 200:

Meanwhile, recent market darling DroneShield continues to descend faster than one of its targets on the battlefield:

The Australian dollar is worth 64.84 US cents but a whopping 101.94 Japanese yen.

Japanese bond market flashing red

The Japan 10-year government bond yield has just hit 1.83%, up 7 basis points or 0.07%.

It’s the highest it has been since the onset of the global financial crisis in 2008.

The Japanese bond market acts like a magnet for offshore funds — the higher it goes, the more money heads to Japan.

Wall Street, one could say, would prefer that money stay in the US.

One Australian dollar is now buying 101.94 yen, up 1.2%. That’s a 12-month high.

Beyond Nvidia: the biggest question in global finance

It’s worth keeping an eye on the global bond market.

In particular, the Japanese bond market is worth examining.

Today the Japanese 10-Year government bond yield is up 3 basis points (0.03%) to 1.79% at 2:20pm AEDT.

Earlier today Japan’s 10-year government bond yield climbed above 1.8% — its highest level since 2008.

Investors are anticipating an announcement from newly minted Prime Minister Sanae TakaichI about her multi-trillion-yen fiscal stimulus package.

The bigger it is, the more Japanese government bonds will need to be sold to finance it.

Hundreds of billions of dollars have left Japan in recent years and made their way into the US government bond market and US equities (shares).

The carry trade has seen investors borrow money from Japan at a low cost and invest that money in the US.

Analysts say there will come a point when Japanese interest rates make this trading strategy unfeasible.

When this happens there may be a capital flight out of the US and Europe and back to Japan.

Where that yield (rate) is, to encourage this trade, is the $1 trillion question.

“We are waiting with bated breath to see when capital will be repatriated from offshore into Japan,” Jamieson Coote Bonds’ Charlie Jamieson told ABC News.

Blog community

Yes, I’d agree with that Matthew. The fact that 50% of the NASDAQ valuation consists of half-a-dozen companies who are all chasing the same end market and essentially basing their forecasts on sales to each other is insane. The end market will probably sustain only one of them. So there goes 40% of NASDAQ valuation.

(p.s. Declaration :- I called my Broker (Merrill Lynch) two days before the crash of 1987 and told him what would happen. I have bought out-of-the-money January Put options on the NASDAQ Index.)

– Stan

I’m thrilled you finance whizzes are sharing thoughts on the ABC biz blog.

You rock.

Australians spend up on utilities and telecoms

The National Australia Bank (NAB) is pumping out the research today.

It’s released its new ‘Consumer Spend Trend’ (October 2025) report.

Here’s an excerpt:

Over the past year:

- Total consumer spending rose 7.1%, marking a slowdown from the 8.0% growth rate recorded in September.

- Spending on utilities & telecoms led the growth in the year to October after the end of energy bill rebates.

- Spending also increased significantly in discretionary categories, including personal goods and hospitality.

The AI end game

Stan, might make sense to read the earnings reports.

Nvidia are currently not projecting any sales to China at all in their figures. They have more than enough demand from the likes of Microsoft, Google, Amazon, Oracle and Meta. They are literally sold out in many instances.

The figures from Nvidia are not what you need to worry about. The real worry is whether Nvidia’s customers will be able to generate enough revenue to justify all the hardware they will deploy.

– Matthew

Well put, Matthew.

RBA lacks clarity on crucial economic signals

The Reserve Bank desperately wants to know how to measure the economy’s capacity or, more specifically, it’s amount of spare capacity.

This can inform the central bank on whether aggregate demand in the economy equals aggregate supply.

This in turn tells the RBA if, for example, demand is greater than supply, that price increases are likely to grow in magnitude.

In addition, the Reserve Bank lacks insight into business’ willingness to pass on higher costs to customers.

This would also inform the bank’s perspective on the present inflation threat.

Earlier today, RBA chief economist, Sarah Hunter, spoke about this.

Here’s an excerpt of her remarks:

A particular focus of our work on inflation dynamics is to understand whether businesses have changed the way they set prices since the pandemic. Do firms now look to pass costs through more quickly, if they can, given the recent experience of high inflation? How do firms’ profit margins vary as economic conditions change?

To get a handle on these questions, we are making use of microdata sets from the Australian Bureau of Statistics (ABS) that allow us to look at anonymised individual firms’ pricing decisions. We’re hopeful that this research will tell us more about how businesses respond as their costs and conditions change, which will ultimately add to our understanding of inflation.

A second topic we’re currently focused on is the economy’s supply capacity. As my colleague Deputy Governor Hauser recently discussed, the Monetary Policy Board is focused on setting monetary policy to keep demand in the economy in line with potential supply. If we can sustain this over time and expectations remain anchored, inflation will be within our 2–3 per cent target band and the labour market will be sitting at full employment.

Road users’ budgets squeezed: CreditorWatch

Here’s a note from CreditorWatch on the road transport sector:

- Operators are being squeezed by higher fuel and finance costs, low profit margins, driver shortages, regulatory complexity and intense price competition – much of it from low-cost or foreign-backed entrants.

- Business closure rates in the road transport sector are now approaching those of the notoriously volatile hospitality sector, posing mounting risks for any business reliant on road freight transport.

- Key warning signs include a sustained increase in invoice payment defaults (up 99.1% year-on-year) and a surge in companies carrying large ATO tax debts.

- The ACT saw the highest closure rate in the sector (14.52%) over the past 12 months with Western Australia faring best at 5.71%.

Economy bursting… in slow motion: NAB

The National Australia Bank specialises in business banking.

As such, its business surveys are well regarded and studied by the Reserve Bank.

It’s November “Forward View — Australia” is featured below.

In really simply terms, the NAB is saying the Australian economy is, despite only producing below-trend growth, bursting at the seams.

The capacity of the economy to grow, needs to improve, or stronger demand will produce further inflation.

In other words, Australia’s productivity needs to lift, urgently.

Overall, we continue to see a relatively soft landing for the economy, with only small tweaks to our 2026 growth forecast (slightly softer) and unemployment rate (slightly higher) forecast over the past month. Q3 inflation data was stronger than the RBA’s expectations and confirmed a material and broad-based acceleration from its H1 2025 pace. We expect underlying inflation above 3% for the next couple of quarters, before easing back into the target band and moderating a little further to 2.5% over 2027.

With economic growth expected to sustain near trend, the unemployment rate to remain low, but a less benign inflation back drop, we see the RBA on hold at 3.6% for the foreseeable future. Abstracting from a negative global shock, the key risk for the RBA and the interest rate outlook is clearly that capacity constraints broaden or intensify.

Indeed, the latest NAB Business Survey for October show that business conditions increased further in the month, and that capacity utilisation remains well above its long-run average. Encouragingly, input cost growth, as well final product price inflation, are tracking around their long-run averages. Early evidence of margin expansion may pose some threat to this benign outcome.

Data over the next couple of months will be crucial in assessing how underlying trends in the economy are progressing on the demand side following the volatility in key data points over recent months.

Though dated, the Q3 national accounts (where we expect overall growth of 0.5% qoq) will provide an updated and complete picture of household sector dynamics including income growth, as well a broader perspective on growth– including dwelling and business investment. Fresh reads for the labour force survey and household spending will provide greater clarity around the ongoing (or otherwise) resilience and capacity of the labour market as the impact of private sector activity flows through, and the durability of the consumer recovery. The first full monthly CPI is released next week and will provide a more granular picture of recent inflation trends amid the spike in Q3.

Nvidia’s P/E

I’ll see Your VanEck analyst and raise you one scary fact.

Nvidia are already trading on a PE of over 50x.

The PE of Wall Street immediately before the crash of 1929 was……..

30x.

– Stan

Stan,

I wouldn’t dream of calling your bluff.

Thanks for the comment.

DT

Iron Ore price back on the board

Is there a reason ,iron oreprices,are not being posted

– Bryan

An oversight, Brian.

Our apologies.

DT

Market snapshot

- ASX 200: +0.9% to 8,529 points

- Australian dollar: +0.1% to 64.83 US cents

- Wall Street: Dow Jones (+0.1%), S&P 500 (+0.4%), Nasdaq (+0.6%)

- FTSE 100: -0.5% to 9,507

- XETRA DAX: -0.1% to 23,162 points

- EuroStoxx 600: FLAT at 561 points

- Spot gold: +0.2% to $US4,090/ounce

- Oil (Brent crude): +0.3% to $US63.70/barrel

- Iron Ore: FLAT at $US104/tonne

- Bitcoin: +1.1% to $US92,497

Prices current around 12:45pm AEDT

{kind=link}